For the past two years, the global tech investment community has focused almost exclusively on massive AI data centers.

Companies producing high-end graphics processing units (GPUs), High Bandwidth Memory (HBM), and advanced AI servers have rightfully attracted enormous capital as hyperscale cloud providers aggressively expanded their infrastructure footprint.

However, another monumental technological transformation is quietly unfolding in the background.

Artificial intelligence is aggressively moving away from centralized cloud architectures and directly into consumer-level personal hardware.

Instead of routing every single AI prompt or compute request to a remote server farm, the next generation of smartphones, laptops, tablets, and edge devices will increasingly process complex AI workloads locally.

This pivotal technological shift is known as On-Device AI, and it is poised to ignite a completely fresh investment cycle for a broad array of semiconductor suppliers, advanced packaging firms, high-density PCB manufacturers, thermal management innovators, and sub-layer substrate producers.

Rather than obsessing only over hyper-inflated AI chip design stocks, forward-looking investors stand to benefit deeply from understanding which critical component suppliers are positioned to capture the value from this next inevitable phase of AI adoption.

Understanding the Mechanics: What Exactly Is On-Device AI?

Traditional artificial intelligence applications rely entirely on the heavy lifting of cloud servers. When a user queries an AI assistant, auto-generates code, or renders an image, the underlying computational heavy lifting occurs thousands of miles away inside an industrial-scale data center.

On-Device AI completely upends this dependency model. Instead of processing software commands remotely, a significant portion of AI execution takes place natively on the silicon of the smartphone, laptop, or tablet itself.

Key real-world applications driving this shift include:

- Real-time, zero-latency multi-language voice translation

- Natively integrated, advanced on-device photo and video editing

- Context-aware, deeply personalized local AI assistants

- Advanced computer vision and intelligent camera systems

- Secure, completely offline generative AI functionality

- AI-driven, micro-level hardware and battery performance optimization

This localized approach dramatically slashes data latency, ensures institutional-grade user privacy, and massively lowers the compounding electricity and computing costs of cloud infrastructure.

One structural factor that deserves far more investor attention is the absolute scale: while the AI server market is measured in millions of units, the consumer electronics market spans billions of active individual devices that will eventually require dedicated AI hardware overhauls.

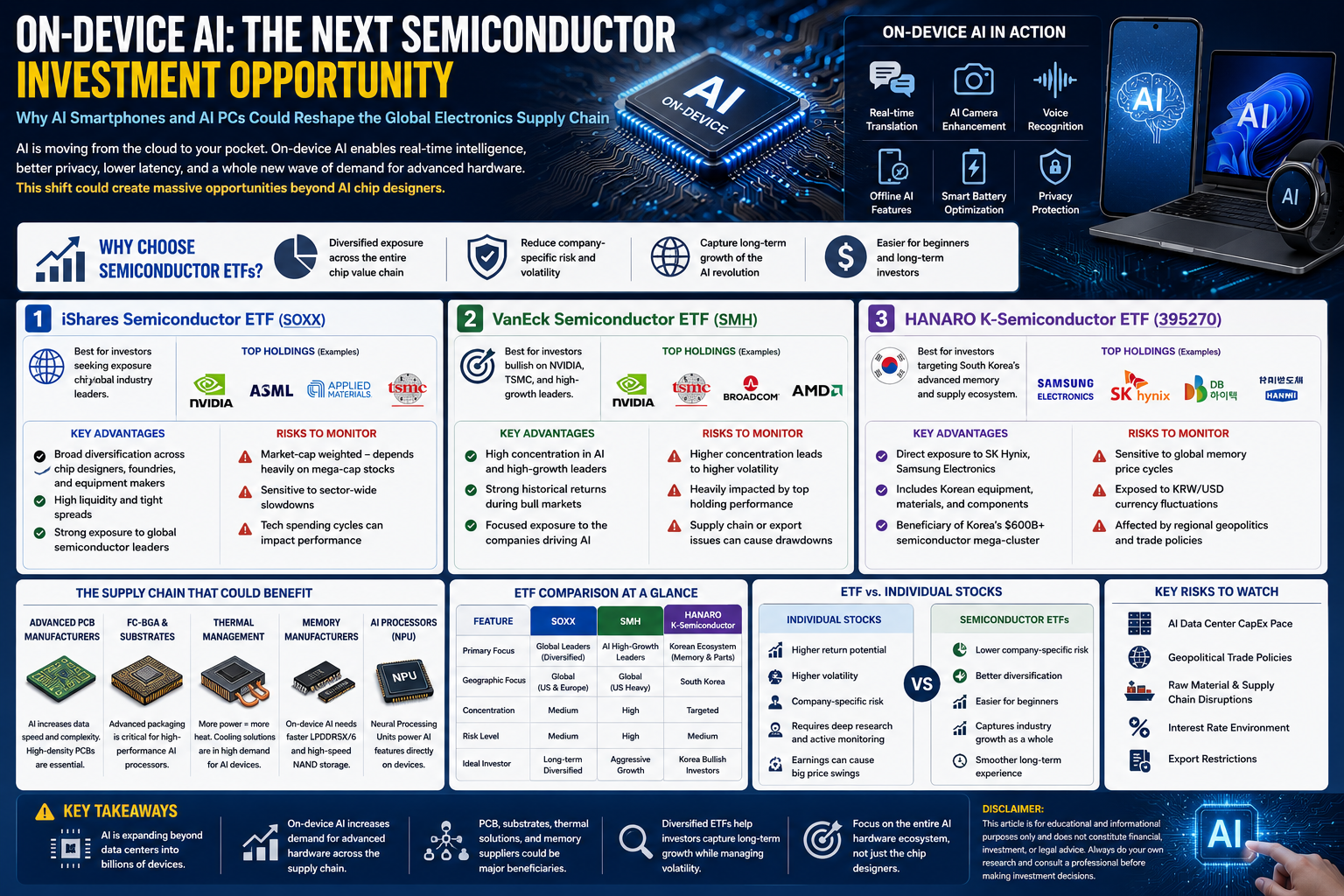

The Strategic Supply Chain Tailwinds for Investors

A common mistake among retail capital allocators is assuming that the entire growth horizon of AI begins and ends with companies building hyperscale data centers. That assumption is rapidly becoming obsolete.

As local AI integration transitions into a non-negotiable baseline standard for consumer tech, device OEMs will be forced to stuff significantly more expensive, premium hardware inside every single chassis they manufacture.

Future-ready AI smartphones and AI PCs require a substantial component upgrade cycle, structurally boosting demand for:

- Hyper-fast mobile application processors

- Dedicated hardware NPUs (Neural Processing Units)

- Expanded, high-bandwidth system DRAM layouts

- Larger, ultra-fast enterprise-grade NAND flash arrays

- Sophisticated, highly efficient thermal management systems

- Denser, high-layer count printed circuit boards (PCBs)

- Ultra-premium semiconductor packaging substrates

Consequently, On-Device AI is not just a tailwind for a single luxury chip brand; it represents a tide that lifts the financial boats of the entire global electronics manufacturing ecosystem.

4 Critical Sectors Set to Benefit from the Edge-AI Boom

1. High-Density Advanced PCB Manufacturers

Artificial intelligence dramatically intensifies the sheer volume of data packets moving between microprocessors. Higher local processing speeds require highly sophisticated, multilayer Printed Circuit Boards (PCBs) capable of supporting hyper-fast signal transmission without experiencing signal degradation.

Fabricators specializing in High-Density Interconnect (HDI) technologies and ultra-thin multilayer board configurations are staring at multi-year margin expansions as consumer electronics design complexities skyrocket.

2. FC-BGA and Next-Gen Advanced Substrate Suppliers

Modern localized AI computing architectures are entirely dependent on advanced semiconductor packaging. Flip Chip Ball Grid Array (FC-BGA) substrates play a vital role, connecting dense processing units to the mainboard while supporting massive data transfer bandwidth.

As on-device neural chips become more complex, substrate precision becomes paramount. Premium edge-AI processors require more internal layers, enhanced thermal resistance, and flawless signal integrity. Historically, even minor shortages in advanced substrates have delayed entire global consumer device rollouts.

3. Precision Thermal Management Companies

Running complex language models locally pushes mobile and laptop processors to their absolute limits. More concentrated compute density inevitably translates to extreme heat.

Because thermal throttling can instantly destroy user experience, this shift opens massive revenue pipelines for specialist firms developing:

- Ultra-thin consumer vapor chambers

- Advanced graphite cooling sheets

- High-conductivity thermal interface materials (TIM)

- Custom micro-cooling modules

4. Market-Leading Memory Manufacturers

On-Device AI demands a profound increase in local volatile memory. To seamlessly run large language models (LLMs) locally without internet latency, consumer devices require massive upgrades to:

- LPDDR5X and next-generation LPDDR6 mobile architectures

- High-speed, dense NAND flash modules

This secular trend acts as an outstanding catalyst for established memory conglomerates that currently dictate the boundaries of global silicon production.

Institutional Anchors: Key Global Giants Driving the Paradigm Shift

Qualcomm

Qualcomm commands a powerful position in mobile AI processing via its Snapdragon platform. It remains the absolute primary engine driving generative AI functionality across premium Android smartphone ecosystems worldwide.

Apple

Apple continues to aggressively scale its local machine learning capabilities by embedding increasingly powerful Neural Engines directly into its custom-designed Apple Silicon. Their tightly integrated hardware-software ecosystem is uniquely optimized to drive mass consumer adoption of local AI features.

Samsung Electronics

Samsung operates as a uniquely positioned titan, housing advanced consumer device development, global memory chip market share, display manufacturing, and foundry fabrication capabilities under one roof. This sheer vertical integration provides unmatched structural advantages as local AI components commoditize.

SK Hynix

As device manufacturers demand higher-capacity, ultra-efficient mobile DRAM to feed local AI models, SK Hynix is positioned to leverage its absolute dominance in premium memory architectures to secure highly profitable tier-1 supplier contracts.

TSMC

Ultimately, nearly every major fabless AI processor designer on earth relies completely on TSMC’s bleeding-edge foundry nodes for actual physical manufacturing. As local hardware specifications tighten, TSMC’s manufacturing monopoly remains a premium portfolio cornerstone.

Cross-Sector Opportunities Breakdown

Hardware Segment Primary Strategic Role Industry Growth Potential AI Processing Units (NPUs) Natively executing local algorithmic tasks High (Direct structural demand) High-Density PCBs Sustaining clean, hyper-fast local data transmission Medium-to-High (Premium margin expansion) Advanced FC-BGA Substrates Enabling ultra-precise packaging for modular chips High (Crucial manufacturing bottleneck) Next-Gen Mobile Memory Housing and cycling localized machine learning models High (Mandatory volume upgrade) Thermal Cooling Solutions Preventing hardware degradation via heat dissipation Medium-to-High (Rapidly growing accessory market)

Macro Risks and Structural Bottlenecks to Monitor

While the long-term investment framework for local AI hardware is exceptionally bullish, prudent capital allocators should map and monitor several structural risks:

- Consumer Replacement Velocity: The broader hardware market relies heavily on consumers being willing to accelerate their normal smartphone and laptop upgrade cycles specifically to access AI software features.

- Component Supply Inbalances: Rapid capacity expansions across specialized packaging or chemical inputs can occasionally lead to short-term oversupply dynamics, temporarily dampening commodity pricing power.

- Regulatory and Trade Crosswinds: Evolving international trade policies, regional microchip subsidies, and strict cross-border export restrictions continue to challenge supply chain forecasting models.

My Investment View & Strategic Conclusion

In my view, On-Device AI represents the absolute most logical, high-probability growth frontier for the global semiconductor space following the explosive initial buildout of AI server data centers.

While cloud-based supercomputing will always remain highly relevant for massive corporate tasks, the monetization of billions of everyday consumer smartphones, laptops, and smart edge devices represents an exponentially larger long-term total addressable market (TAM).

The most vital observation that mainstream investors miss is that an AI device requires a massive network of supporting technologies to function efficiently. A high-performance NPU is practically useless without upgraded memory channels, advanced multilayer circuit boards, ultra-precise packaging substrates, and high-efficiency thermal cooling systems.

Therefore, instead of chasing overvalued, high-profile chip designers trading at extreme valuation multiples, smart investors can find incredibly attractive, structurally sound entry points among the specialized supplier networks feeding the broader hardware ecosystem. In the grand scheme of the technology revolution, investing in the essential building blocks of the device infrastructure remains the ultimate defensive growth strategy.

Frequently Asked Questions (FAQ)

1. Will On-Device AI eventually replace Cloud-based AI systems?

No. The general consensus among industry experts is a hybrid coexistence model. Massive, heavy-compute algorithmic tasks will remain anchored to hyperscale cloud infrastructure, while everyday productivity tasks, privacy-sensitive workflows, and instant-response queries will handle natively on the device.

2. Why does local AI require so much more device memory (DRAM)?

Unlike traditional applications, running a localized Large Language Model (LLM) requires the model’s parameters to remain constantly loaded into the system’s volatile memory for instant processing. Without a massive jump in DRAM capacity, the device will experience crippling performance bottlenecks.

3. How can retail investors target the substrate and packaging segments safely?

Beyond choosing individual micro-cap suppliers, looking into specialized technology ETFs that explicitly capture global semiconductor equipment, materials, and advanced packaging indexes is an excellent way to diversify exposure across this critical chokepoint.

Disclaimer: This article is published strictly for educational and informational purposes only. It does not constitute formal financial, professional, or investment advice. Allocation of capital inside technology sectors involves notable market volatility; always conduct your own extensive research and consult a licensed professional before making financial allocations.