The global electric vehicle (EV) market has officially entered a new, structural phase.

Instead of asking, “Which EV manufacturer will win the market share war?”, smart investors are now pivoting to a much more lucrative question: “Who supplies the core technology that every single EV company absolutely needs?”

The answer almost always leads straight to battery material manufacturers.

Among them, cathode material companies occupy the most critical strategic position in the entire battery supply chain. Unlike individual EV brands that face intense competition and price wars against one another, battery material companies possess the unique ability to supply multiple automakers simultaneously. This creates highly diversified revenue streams and provides far more stable, long-term compounding growth.

This comprehensive guide examines three of South Korea’s largest cathode material giants from an institutional investor’s perspective.

Rather than simply introducing each company, we will deeply analyze where their sustainable competitive advantages come from, the specific macroeconomic risks they face, and how they are positioned to capture massive future trends—such as Next-Generation EVs, Energy Storage Systems (ESS), and AI data center power infrastructures.

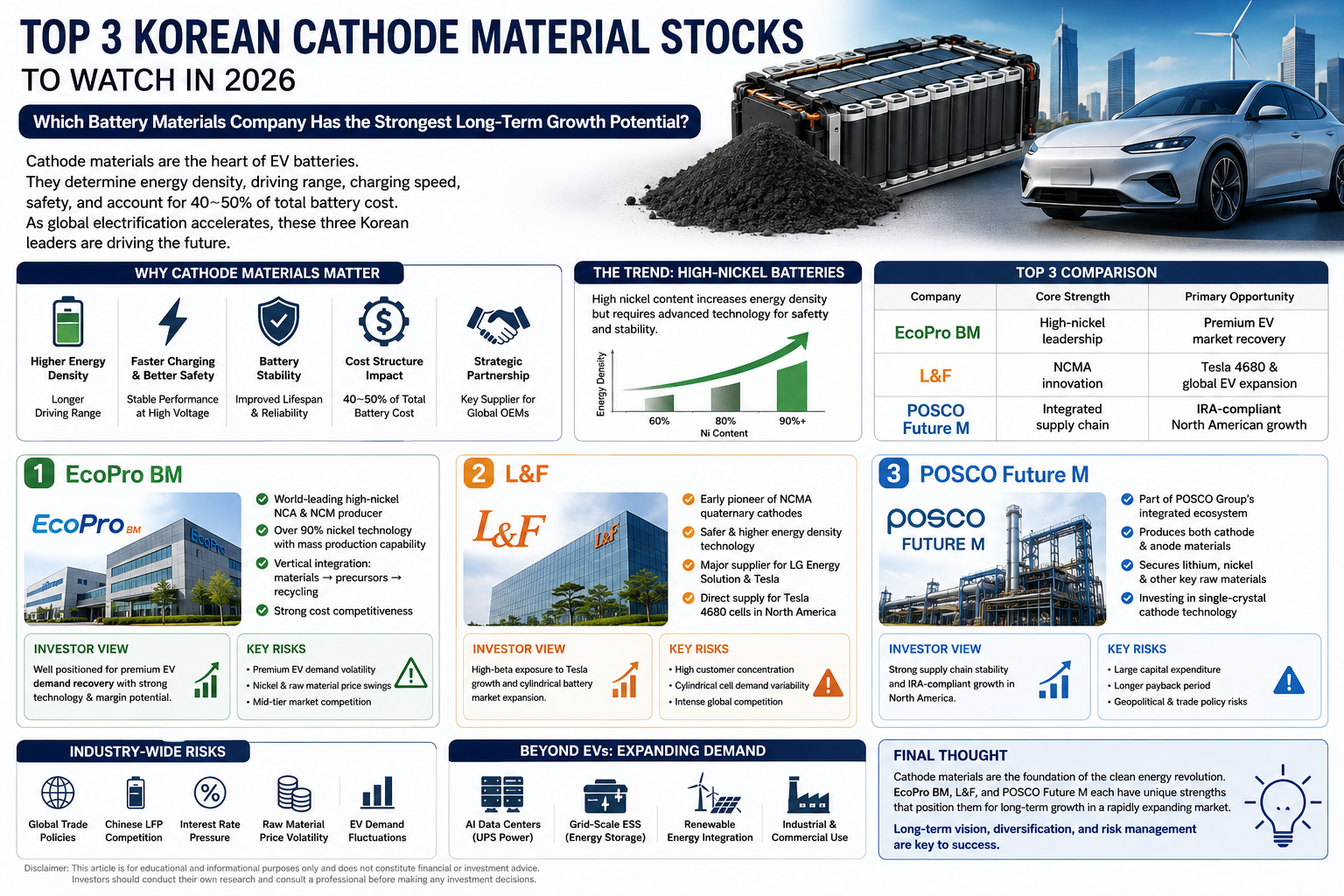

Why Cathode Materials Matter More Than Many Investors Realize

When retail investors first begin studying lithium-ion batteries, they usually make the mistake of focusing strictly on spot lithium prices. However, global battery manufacturers and tier-1 automakers pay much closer attention to the quality of the cathode materials.

Why do cathodes dictate the entire battery industry?

Because the cathode chemical composition largely determines the absolute core metrics of the vehicle:

- Battery Capacity & Driving Range: Higher energy density allows vehicles to travel significantly farther on a single charge.

- Charging Speed & Safety: Advanced structures prevent degradation during ultra-fast charging cycles.

- Manufacturing Cost: In a standard EV battery pack, cathode materials alone account for approximately 40% to 50% of total cell production costs.

This means that even minor incremental improvements in cathode engineering can drastically enhance an automaker’s profitability. Consequently, companies capable of consistently mass-producing high-performance cathode materials become indispensable strategic partners for global OEMs.

The Dominant Market Trend: High-Nickel Batteries in 2026

Battery technology has evolved at a breakneck pace over the past decade. While earlier EV batteries heavily prioritized basic chemical stability, today’s premium electric vehicles demand an uncompromising combination of extended driving range, rapid charging speeds, and lighter battery packs.

These commercial requirements have rapidly accelerated the global adoption of High-Nickel Cathodes.

Increasing the nickel content within a cell directly boosts its energy density. However, doing so introduces severe engineering challenges, primarily regarding thermal stability and complex manufacturing chemistry. As a result, the select few companies that have successfully mastered the balance between high energy density and optimal safety are expected to hold a near-impenetrable technological monopoly.

Core Company Analysis 1: EcoPro BM (KOSDAQ: 247540)

The Structural Competitive Advantage

EcoPro BM has firmly established itself as the world’s leading high-nickel cathode producer by volume and technological scale. Unlike competitors who specialize in only a single chemical profile, EcoPro BM boasts a versatile portfolio, producing both NCA (Nickel-Cobalt-Aluminum) and NCM (Nickel-Cobalt-Manganese) configurations.

Its primary technological moat lies in its proven ability to mass-produce cathodes containing over 90% nickel while maintaining strict quality consistency across millions of units.

Furthermore, their greatest long-term operational advantage is vertical integration. Rather than depending entirely on volatile third-party suppliers, the parent company, EcoPro, has established a closed-loop ecosystem. This internalizes everything from precursor manufacturing and lithium refining to battery recycling, significantly cushioning profit margins during periods of raw material price volatility.

The Investor’s Perspective

From a valuation standpoint, EcoPro BM is the ultimate benchmark play on the premium EV market’s recovery. Their technological leadership allows them to command higher premium profit margins compared to commodity-grade battery material producers.

Key Risks to Monitor

- High concentration and exposure to cyclical premium EV consumer demand.

- Sudden fluctuations in international nickel and cobalt spot prices.

- Rising competition in the mid-tier market from low-cost alternatives.

Core Company Analysis 2: L&F (KOSE: 066970)

The Structural Competitive Advantage

L&F became an internationally recognized powerhouse through its early, aggressive commercialization of NCMA (Nickel-Cobalt-Manganese-Aluminum) quaternary cathodes. By adding aluminum to the high-nickel molecular structure, L&F successfully enhanced thermal stability and structural safety while maintaining exceptional energy density.

This breakthrough chemistry immediately attracted global tier-1 cell makers seeking a safer way to power next-generation, high-performance EVs.

The Tesla Connection & Investor’s Perspective

L&F offers the most direct, high-beta exposure to Tesla’s global delivery volume. The company is deeply embedded in the supply chain for LG Energy Solution’s cylindrical cells, which directly supply Tesla’s Gigafactories in Shanghai and Berlin.

More importantly, L&F bypassed traditional intermediaries to secure direct, multi-billion-dollar supply contracts with Tesla for its in-house 4680 cell production lines in North America. For investors who believe in Tesla’s long-term production scaling, L&F acts as a highly leveraged play on that exact growth.

Key Risks to Monitor

- High customer concentration risks tied heavily to Tesla and LG Energy Solution’s performance.

- Vulnerability to short-term changes in cylindrical battery adoption rates.

- Intense global competition within the North American subsidy framework.

Core Company Analysis 3: POSCO Future M (KOSE: 003670)

The Structural Competitive Advantage

POSCO Future M offers a fundamentally different, highly defensive investment thesis. Instead of operating purely as a chemical engineering firm, the company benefits immensely from the massive industrial powerhouse that is the POSCO Group.

POSCO Future M is the only player in South Korea capable of manufacturing both cathodes and anodes (graphite/silicon-based negative active materials) simultaneously.

The Ultimate Supply Chain Moat

Investors seeking unparalleled structural stability often favor POSCO Future M. Because the POSCO Group directly owns actual lithium brine lakes in Argentina, nickel mining operations in Indonesia, and domestic processing plants, POSCO Future M possesses ironclad raw material sovereignty.

This makes them an exceptionally attractive, fully IRA-compliant partner for North American OEMs like General Motors (through their massive Ultium Cells joint venture). Furthermore, their aggressive investments in single-crystal cathode technology aim to radically improve battery lifespans and eliminate thermal risks entirely.

Key Risks to Monitor

- Massive, ongoing capital expenditures (CapEx) compressing short-term free cash flow.

- A longer investment recovery period compared to pure-play peers.

- High reliance on the broader geopolitical trade policies between the US, EU, and Asia.

Comparing the Korean Cathode Giants

Company Core Strategic Moat Primary Growth Catalyst Ideal Investor Profile EcoPro BM Ultra high-nickel volume scale Premium EV market recovery Bullish on global market-share leadership and pure tech margins. L&F Direct Tesla supply & NCMA innovation Tesla 4680 & cylindrical cell ramp-up Seeking high-beta exposure directly tied to Tesla’s ecosystem. POSCO Future M Complete vertical raw material integration Long-term IRA-compliant North American expansion Long-term compounding investors valuing supply chain monopolies.

Rather than trying to guess which individual stock is universally “best,” smart investors should evaluate which specific business model and supply chain profile aligns closest with their personal risk tolerance and macroeconomic outlook.

Industry-Wide Risks Facing the Battery Sector

Even the structurally strongest businesses do not operate in a vacuum. Investors allocating capital into the battery materials space must continuously monitor several macroeconomic headwinds:

- Global Trade Policies & Tariffs: Ongoing adjustments to the US Inflation Reduction Act (IRA) and European subsidy frameworks can abruptly alter supply chain values.

- Chinese LFP Competition: The rapid global expansion of lower-cost Lithium Iron Phosphate (LFP) cells forces premium manufacturers to continuously innovate.

- Macro Economic Pressures: Sustained high interest rates can temporarily slow down consumer adoption of big-ticket items like premium electric vehicles.

The Macro Outlook: Expanding Beyond Electric Vehicles

In my opinion, the long-term secular outlook for premium cathode material companies remains incredibly attractive because the market often forgets one critical factor: Electric vehicles are not the only source of battery demand.

As the global economy digitizes and transitions to clean energy, high-performance battery materials are increasingly being deployed across massive secondary markets:

- AI Data Centers: Requiring massive, uninterrupted power supply (UPS) systems to prevent computational downtime.

- Grid-Scale Energy Storage Systems (ESS): Essential for storing intermittent solar and wind energy on global power grids.

- Commercial & Industrial Battery Arrays: Replacing traditional backup diesel generators worldwide.

These massive, non-automotive sectors provide a powerful structural safety net, significantly reducing these companies’ total dependence on passenger EV sales alone. While battery material stocks are historically volatile, their position as the fundamental gatekeepers of electrification makes them an essential cornerstone of modern tech investing.

Frequently Asked Questions (FAQ)

1. Why are cathode materials considered the most important battery component?

They directly dictate an EV’s maximum driving range, energy density, charging speed, and overall safety profile, while making up roughly 40% to 50% of the total battery cell production cost.

2. Is a higher nickel content always better for a battery?

Not necessarily. While higher nickel content drastically increases energy density and driving range, it introduces high chemical volatility and manufacturing complexity. Mastering the safety of high-nickel chemistry is what separates industry leaders from commodity producers.

3. Which Korean company possesses the best technology?

Each titan specializes in a different structural strength:

- EcoPro BM leads the world in sheer high-nickel NCA/NCM production volume.

- L&F pioneered safer, cost-effective NCMA quaternary chemistry heavily used by Tesla.

- POSCO Future M owns an unbeatable global monopoly over raw material integration and supplies both anodes and cathodes.

Disclaimer: This article is published strictly for educational and informational purposes only. It does not constitute financial, legal, or investment advice. Investors must conduct their own thorough due diligence and consult with a certified financial professional before making any capital allocations.