Artificial intelligence is reshaping the global semiconductor industry at an unprecedented pace.

The rapid expansion of AI infrastructure, cloud computing architectures, autonomous vehicles, and high-performance computing (HPC) has dramatically accelerated global demand for advanced memory chips and scalable semiconductor manufacturing capacity.

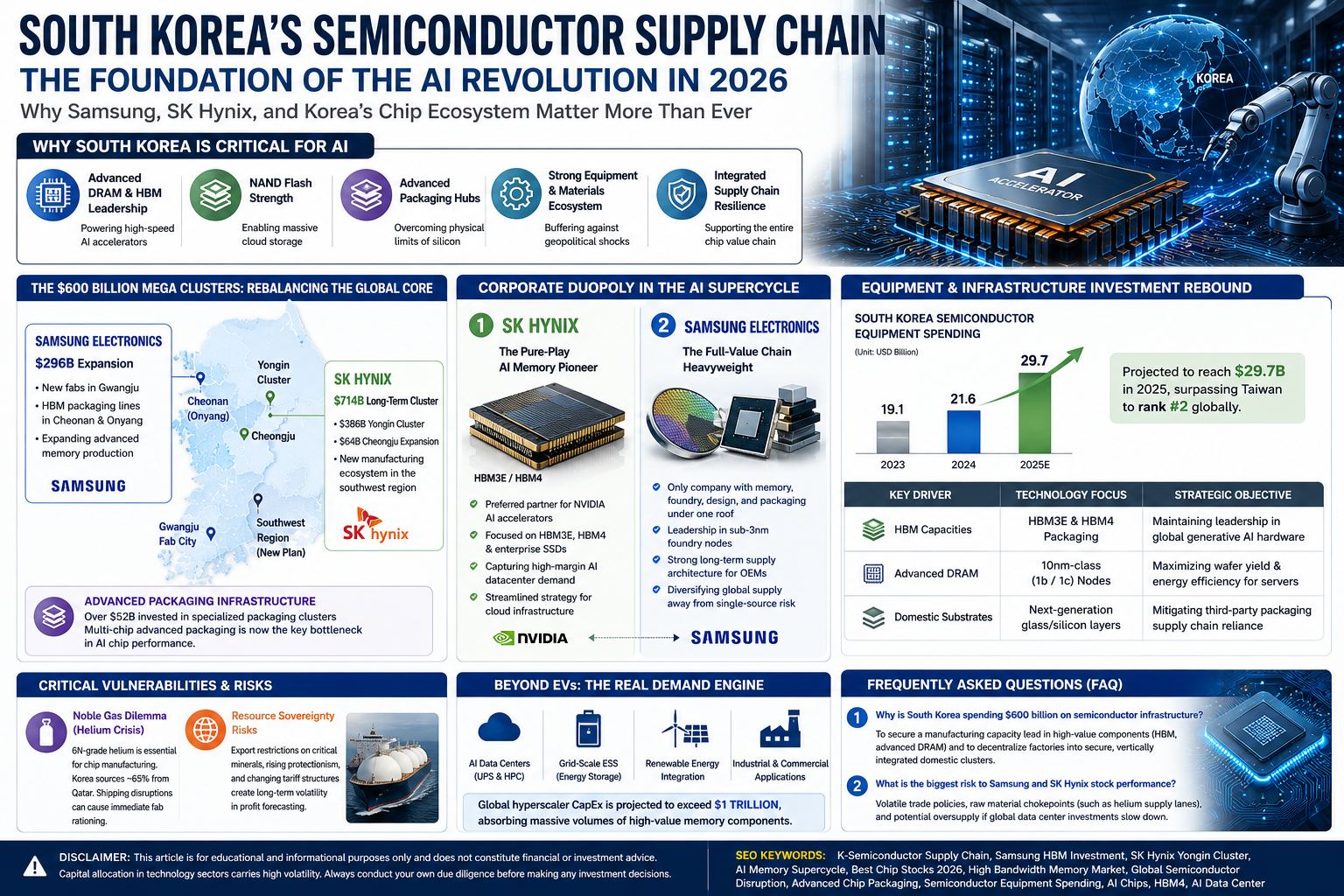

As a result, South Korea has firmly cemented its position as one of the world’s most strategically indispensable semiconductor hubs.

For many casual retail investors, semiconductor companies are still incorrectly associated only with traditional smartphone or personal computer (PC) replacement cycles. However, this outdated macroeconomic view is quickly becoming obsolete.

Today, the industry’s real long-term growth engine is increasingly driven by AI training servers, hyperscale cloud data centers, advanced multi-chip packaging technologies, and next-generation memory profiles—such as High Bandwidth Memory (HBM).

One critical point that deserves immediate attention from investors is that the current AI boom is not benefiting every semiconductor company equally.

Companies with deeply entrenched positions in high-speed memory architectures, advanced turnkey packaging, and fully integrated manufacturing ecosystems appear positioned for disproportionate revenue windfalls compared to businesses focused primarily on legacy, commodity-grade memory chips.

This comprehensive article deeply examines South Korea’s updated semiconductor ecosystem, explains why it plays a gatekeeping role in the global AI supply chain, and provides an institutional analysis of how Samsung Electronics and SK Hynix are positioning themselves for the next decade of structural growth.

Why South Korea Plays a Critical Role in the AI Revolution

Operating and training massive artificial intelligence models requires an astronomical amount of computing power. Training large language models (LLMs) and running real-time generative AI services depend not just on powerful graphics processing units (GPUs), but also on hyper-fast memory solutions and flawless semiconductor fabrication processes.

While global technology titans like NVIDIA or AMD design the underlying AI processors, they rely heavily on specialized Asian semiconductor ecosystems to actually manufacture, assemble, and package these ultra-dense chips efficiently.

South Korea has successfully developed one of the world’s most resilient semiconductor supply chains, structurally reinforced by:

- Advanced DRAM Manufacturing: Mass-producing 10-nanometer class nodes that offer high data-processing efficiency.

- High Bandwidth Memory (HBM) Monopolies: Dominating the world’s supply of low-latency, stacked memory components essential for AI accelerators.

- NAND Flash Production Leadership: Driving high-capacity enterprise Solid State Drives (eSSDs) required for massive cloud storage arrays.

- Advanced Semiconductor Packaging Hubs: Overcoming physical silicon limits through multi-die integration and modern packaging substrates.

- Localized Materials & Equipment Ecosystems: Maintaining a tight-knit network of specialized domestic suppliers to buffer against geopolitical trade shocks.

Rather than competing in only one isolated segment, South Korea has built an incredibly integrated, comprehensive ecosystem capable of supporting nearly every crucial stage of memory innovation. From a long-term strategic perspective, this highly diversified supply structure provides far greater operational resilience than relying on a single, isolated technology component.

Korea’s Massive Long-Term Semiconductor Investment Strategy

South Korea continues to deploy unprecedented capital into its domestic semiconductor infrastructure through a heavily coordinated alliance between the central government and private tech conglomerates.

Instead of concentrating all production capacities inside a single region, manufacturers are strategically distributing and expanding mega-scale fabrication facilities across multiple decentralized locations. This nationwide strategy is designed to exponentially boost total production capacity while protecting the supply chain from localized structural failures or infrastructure vulnerabilities.

The primary, high-value investment allocations are flowing directly into:

- Advanced Next-Gen Memory Fabrication: Building cleanrooms for sub-2nm class memory nodes.

- HBM Mass-Production Scalability: Expanding dedicated high-speed testing and stacking lines.

- Advanced Packaging Facilities: Investing billions to master multi-chip modular assembly.

- R&D Innovation Research Centers: Accelerating the timeline toward solid-state and neuromorphic computing.

- Semiconductor Equipment & Fab Infrastructure: Ensuring reliable, independent power and clean water access across all industrial zones.

Another critical factor that many institutional analysts overlook is that these massive capital expenditures are designed not only to increase nominal volume output, but also to radically shorten the development and validation cycles for future, customized AI chips.

As artificial intelligence hardware requirements evolve faster and faster each quarter, this rapid-to-market development capability will become the ultimate competitive moat for tech OEMs looking for a reliable hardware partner.

Comparative Investment View: Samsung Electronics vs. SK Hynix

For global capital allocators looking to gain exposure to South Korea’s chip supply chain, it is vital to contrast the two major titans:

1. SK Hynix: The Pure-Play AI Accelerator Favorite

SK Hynix has positioned itself exceptionally well by capturing an early, highly lucrative technological relationship with NVIDIA. By specializing heavily in advanced HBM3E and next-generation HBM4 packaging, their revenue model responds immediately to the exploding cloud datacenter CapEx. For high-beta growth investors, SK Hynix represents the front lines of pure AI acceleration.

2. Samsung Electronics: The Full-Value Turnkey Giant

Samsung, on the other hand, is an all-encompassing powerhouse. It is the only enterprise in the world that can design system architectures, fabricate chips via its advanced foundry nodes, produce the underlying high-speed memory, and execute full turnkey advanced packaging under one corporate umbrella. While its scaling timeline requires patience, its unparalleled financial scale offers unmatched long-term stability.

Macroeconomic Risks Investors Must Monitor

While the long-term structural tailwinds remain incredibly bullish, the semiconductor industry is inherently cyclical and highly sensitive to global trade dynamics. Prudent investors should actively monitor the following risk factors:

- Raw Material Supply Lanes: Dependence on global imports for critical industrial inputs (such as high-purity chemicals or noble gases) means shipping disruptions can alter fab production schedules.

- Geopolitical Trade Alignments: Shifting international tariff frameworks and regional chip subsidy structures create a volatile regulatory environment for global corporate forecasting.

- Pace of Data Center CapEx: A sustained investment cycle relies completely on tech giants continuing to funnel record budgets into massive AI computing infrastructure.

My Investment View & Strategic Conclusion

In my view, the structural investment thesis for South Korea’s semiconductor supply chain remains highly attractive. The global conversation has permanently shifted away from simple consumer electronics cycles toward a historic, infrastructure-level electrification of data.

Artificial intelligence, massive green energy grids, and localized enterprise cloud architectures all require an exponential volume of premium memory semiconductors.

While the broader stock market will always experience short-term volatility due to macro economic interest rates and shifting sentiment, the fundamental gatekeepers of data processing power cannot be replaced. For long-term investors aiming to construct a structural portfolio geared toward the future of technology, South Korea’s highly integrated semiconductor supply chain represents an essential, non-negotiable cornerstone.

Frequently Asked Questions (FAQ)

1. Why is memory technology so critical for artificial intelligence?

AI microprocessors (GPUs) require data to move at near-instantaneous speeds. Legacy memory creates a processing bottleneck. Advanced memory solutions like High Bandwidth Memory (HBM) solve this issue by stacking memory layers vertically, creating ultra-wide data highways.

2. How does South Korea’s semiconductor approach differ from other regions?

While some regions focus strictly on contract chip fabrication (foundry) or specific processor designs (fabless), South Korea has specialized in establishing a complete, multi-layered monopoly over advanced memory tech, backed by massive, vertically integrated domestic supply ecosystems.

Disclaimer: This article is published strictly for educational and informational purposes only. It does not constitute financial, professional, or investment advice. Capital allocation in technology sectors carries high market volatility; always conduct your own thorough due diligence before making any financial decisions.